Confidence Knocked, Consumers Settle For Unauthorized Loans Amid Covid

Financial health remains tenuous while consumers grounded their needs and empty savings amid rising hospital expenses and dealing to a job loss reveals Way2News survey.

Navigating through the financial impact of a pandemic is Indian consumers’ biggest scare. Covid-19 has touched each of our lives one way or the other and besides health & emotions, managing finances has also been a priority. Covid-19 rooted in for 15 months straight has upended personal and economic lives of many. Triggered financial sentiments, behaviors and the needs of financial decision makers are going to leave consumers blistered for good. But, resurgence in finances has forced many to stricter restrictions.

While experts are alarmed about the measures of Indian consumers to manage finances, India has already battered its savings, and begun migrating to unauthorized/fraudulent loans to absorb pandemic shock, reports Hyperlocal headquarters of India, Way2News. 3 Lakh rural households were surveyed on the financial impact and its stress since the inception of coronavirus in their lives. Here are the takeaways.

1. Consumer confidence takes a knock with zeroed savings. What are the main reasons?

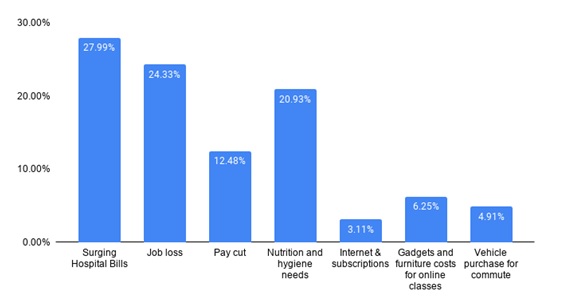

Indian households fell weak, as their current management of running finances shook according to the survey. 28% of households said hospital expenses have surged and 24% of the sample have incurred a job loss that made their financial situation go bonkers. While job loss and pay cuts are a direct impact, consumers might have been left with savings that would cover their expenses for only months to come, which is a very dangerous sign.

On the brighter side(maybe), 21%, a huge number of consumers shelled out money on nutrition and hygiene that significantly affected their finances, quoted the survey. This hints at respondents being accountable and careful. But, that’s a hole in the dent for an average poor household who is shrinking pockets while we are far away from eradicating the virus any time sooner.

To top it off, 12.5% respondents have reported reduced income that is inversely related to the resurging spends, savings and spending. Overall 49% of respondents’ financial schema went haywire already, with upending hospital bills and trying to stay healthy & clean months into the second wave uproar. Remember, consumer confidence is a key aspect of financial recovery and right now it is giving them judders. The lag will directly affect spends and ultimately affect nutrition and protection which might be the scenario in months to come as financial capability of Indians is about to get hit.

2. Desperate times, desperate measures

Out of work: Unauthorized loans, credit from banks and gold collaterals rise significantly

Being stringent and managing finances has been the go-to strategy of 32% of households in India. While picking right and cutting down on non-essentials has helped many breathe during the tough times, another 31.6% of the sample had to-had to touch their savings and utilize them to run an already contracted routine. While this is a great sign of families demonstrating adaptability and resilience, to support this, interestingly, credit and credit card surge(4.9% only) was observed to be very partial in the survey.

And that arose the question, how and where India is heading to borrow some bucks?

For the toughest survival in the history, and the answer was Unauthorized loans and gold collaterals. Right now, consumers are opting for tangible support on credit terms everywhere and that ain’t happening with all the group of households. Finding alternatives were tough and consumers resorted to gold loans, borrowing money at higher interest rates from known, and fraudulent prone loans from various sources that RBI has alarmed us about.

Indians are migrating to instant loan/lending money services, where they get higher limits to borrow, at higher interest. Meaning, lending money by unauthorized lenders at exorbitant interest rates, ending them in a debt trap. 23% have said they have taken this way, already. The question is, How can we control this? And also, can we before it is too late?

Bold measures and stronger crisis management, only vaccine for the long run and India has to work it out, says Raju Vanapala, CEO, Way2News. “With household financial savings contracted, financial distress is rising in every region. If India has to work this out, depleted savings and debt are not going to help consumers as they have a larger potential to impact health and overall wellbeing of household.” added Vanapala when asked about a way out.

While this is the story of an average household in India, what about poor & vulnerably working? People who are out of reach for this sort of survey? Reduce food intake, sell assets, or try to borrow some money? Many states and authorities to curb this awaiting nightmare, are helping people with ration and basic households to not end up in a poverty trap. The truth is, India is unprepared. To help, to educate, to curb or to protect families from an upcoming financial outbreak.

Alternative Titles

1. Battered savings and beefed up loans; The story of India’s Financial Brunt

2. Unauthorized loans, India’s jugaad to burgeoning financial crisis

3. India’s Financial Brunt: An invisible pandemic within a pandemic

4. Confidence knocked, consumers bow down to unauthorized loans for resurging finances amid Covid-19

Highlights

How and where India is heading to borrow some bucks?

- 49% of India’s financial schema scattered with upending hospital bills and trying to stay healthy

- 31.6% of India have utilized their savings, months into the 2nd wave

- Unauthorized loans, credit from banks and gold collaterals rise significantly

- Job loss and pay cuts are a direct impact on households

- Credit and credit card surge to be the least source for financial wellbeing at just 4.9% only

- Consumers are opting for tangible support on credit terms

Indians are migrating to instant loan/lending money services, where they get higher limits to borrow, at higher interest. Meaning, lending money by unauthorized lenders at exorbitant interest rates, ending them in a debt trap. 23% have said they have taken this way, already. The question is, How can we control this? And also, can we before it is too late?

India has to work this out, depleted savings and debt are not going to help consumers says Raju Vanapala, CEO, Way2News